The IRS recently issued its 2026 cost-of-living adjustments for more than 60 tax provisions. The One Big Beautiful Bill Act (OBBBA) makes permanent or amends many provisions of the Tax Cuts and Jobs Act (TCJA). It also makes permanent most TCJA changes to various deductions and makes new changes to some deductions. OBBBA-affected changes have been noted throughout.

As you implement 2025 year-end tax planning strategies, be sure to take these 2026 numbers into account.

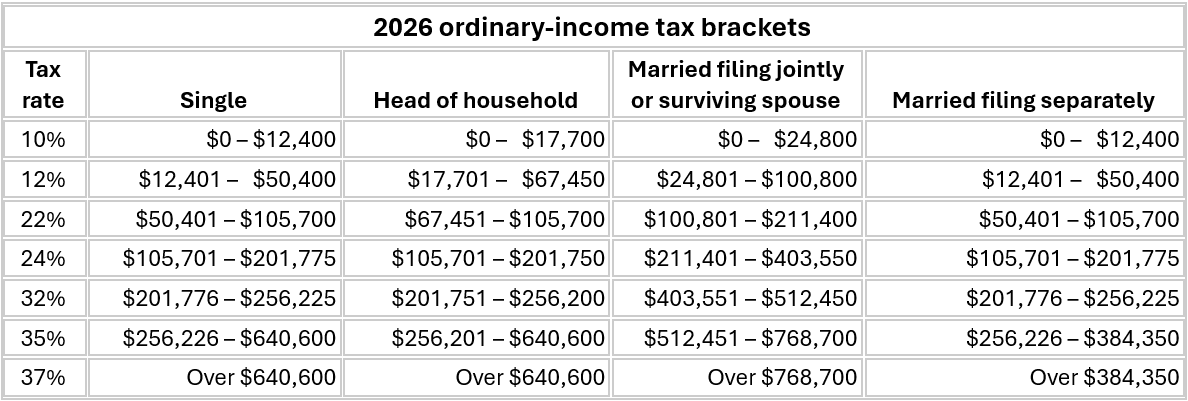

Tax-bracket thresholds increase for each filing status, but because they’re based on percentages, they increase more significantly for the higher brackets. For example, the top of the 10% bracket will increase by $475–$950, depending on filing status, but the top of the 35% bracket will increase by $8,550–$17,100, depending on filing status.

Note that the OBBBA makes the rates and brackets permanent. The income tax brackets will continue to be annually indexed for inflation.

The OBBBA makes permanent and slightly increases the TCJA’s nearly doubled standard deduction for each filing status. The amounts will continue to be annually adjusted for inflation.

In 2026, the standard deduction will be $32,200 for married couples filing jointly, $24,150 for heads of households, and $16,100 for singles and married couples filing separately.

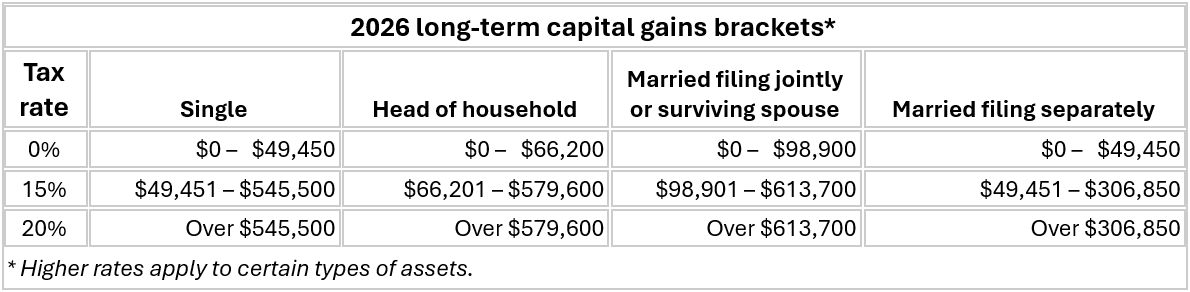

The long-term gains rate applies to realized gains on investments held for more than 12 months. For most types of assets, the rate is 0%, 15% or 20%, depending on your income. While the 0% rate applies to most income that would be taxed at 12% or less based on the taxpayer’s ordinary-income rate, the top long-term gains rate of 20% kicks in before the top ordinary-income rate does.

The alternative minimum tax (AMT) is a separate tax system that limits some deductions, doesn’t permit others and treats certain income items differently. If your AMT liability exceeds your regular tax liability, you must pay the AMT.

Like the regular tax brackets, the AMT brackets are annually indexed for inflation. In 2026, the threshold for the 28% bracket will increase by $5,400 for all filing statuses except married filing separately, which will increase by half that amount.

The AMT exemption amounts were significantly increased under the TCJA. The OBBBA makes the higher exemptions permanent, continuing to index them for inflation. The exemption amounts in 2026 will be $90,100 for singles and heads of households, and $140,200 for joint filers, increasing by $2,000 and $3,200, respectively, over 2025 amounts.

The AMT exemption phases out over certain income ranges. It’s completely phased out if AMT income exceeds the top of the applicable range.

Under the OBBBA, the income thresholds for the phaseout revert to their 2018 levels for 2026 (i.e., removing the inflation adjustments that had been made for 2019–2025) and then will be annually adjusted for inflation again in subsequent years. Also, the OBBBA phases out the exemption twice as quickly beginning in 2026.

So, the exemption phaseout ranges in 2026 will be $500,000–$680,200 for singles and $1,000,000–$1,280,400 for joint filers. These are significantly lower than the 2025 ranges of $626,350–$978,750 and $1,252,700–$1,800,700, respectively.

Amounts for married couples filing separately are half of those for joint filers.

Certain child-related breaks are annually adjusted for inflation but don’t necessarily go up every year. In addition, these breaks are limited based on a taxpayer’s modified adjusted gross income (MAGI). Taxpayers whose MAGIs are within an applicable phaseout range are eligible for a partial break — and breaks are eliminated for those whose MAGIs exceed the top of the range.

Here are the 2026 figures for two important child-related breaks:

The Child Tax Credit. The OBBBA makes permanent the TCJA’s $2,000 per qualifying child credit amount, plus it increases it to $2,200 for 2025. The OBBBA also adjusts the credit annually for inflation starting in 2026. However, because inflation is relatively low and the dollar amount of the credit is relatively small, the credit will remain at $2,200 for 2026. The OBBBA also makes permanent the annual inflation adjustment to the limit on the refundable portion of the credit, but, again, there’s no increase for 2026. The refundable portion will remain at $1,700.

Beware that the Child Tax Credit phases out for higher-income taxpayers, and the phaseout thresholds aren’t inflation-indexed. Under the OBBBA, they’re permanently $200,000 for singles and heads of households, and $400,000 for married couples filing jointly.

The Adoption Credit. The MAGI phaseout range for eligible taxpayers adopting a child will increase in 2026 — by $5,890. It will be $265,080–$305,080 for joint, head of household and single filers. The maximum credit will increase by $390, to $17,670 in 2026. Under the OBBBA, a portion of the credit is refundable, and that portion is annually indexed. For 2026, the refundable portion is $5,120 (up from $5,000 for 2025).

The unified gift and estate tax exemption and the generation-skipping transfer (GST) tax exemption had been scheduled to return to an inflation-adjusted $5 million in 2026. But the OBBBA permanently increases both exemption amounts to $15 million for 2026 and annually indexes the amount for inflation after that.

The annual gift tax exclusion in 2026 remains the same as the 2025 amount: $19,000 per giver per recipient.

With many of the 2026 cost-of-living adjustment amounts trending higher, you may have an opportunity to realize some tax relief next year. However, beware that some taxpayers might be at greater AMT risk because of the reductions to the exemption phaseout ranges. If you have questions on the best tax-saving strategies to implement based on the 2026 numbers, please contact us.

Get in touch today and find out how we can help you meet your objectives.